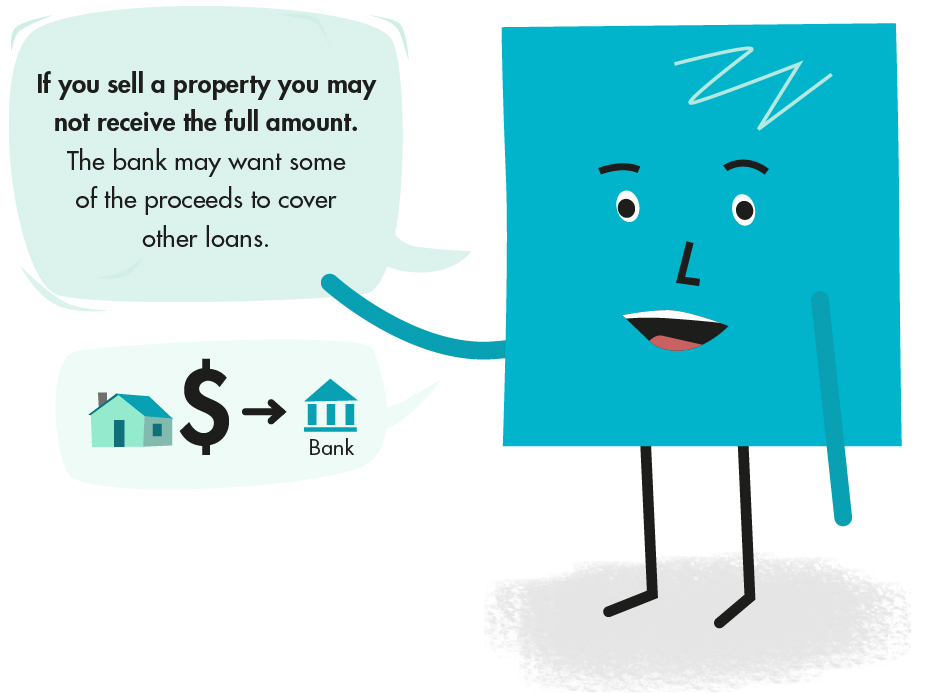

When you sell a property with a mortgage, you can usually keep whatever money is left after repaying the bank loan (unless, of course, you transfer the loan to another property you’ve bought). Things are less straightforward, however, if the mortgage acts as security over more than one loan. In that situation, banks won’t automatically let you keep the entire balance. That’s a source of complaints, as this guide explains.

Existing and future lending

Most mortgages are what’s called an “all obligations” mortgage. This means the mortgage secures all money the property owner may owe the bank, both now and in the future. The result is that it enables the bank to require you to divert the balance on the property you’ve sold towards reducing the amount owed on other loans.

For example, you have two properties. Property A has a mortgage of $300,000 and property B a mortgage of $600,000. Property A sells for $400,000. You want to repay the $300,000 and keep the $100,000. The bank, however, makes you put the $100,000 sale proceeds towards reducing your loan on property B from $600,000 to $500,000. The reason is that it must be satisfied property B provides sufficient security for its remaining loan. In this example, property B might have had a market value of $700,000, which the bank did not consider high enough in view of the $600,000 it was owed. This would have made the loan-to-value ratio 87.7 per cent, hence the need to reduce debt with the proceeds from property A.

Other reasons

A bank may have various reasons for directing that some or all of the proceeds from the sale of one property go towards the loan on another. One, as mentioned, is that the loan-to-value ratio may not be satisfactory on the second loan. Others might be that:

- The bank’s lending criteria may have changed since it approved your loans (the loan-to-value ratio requirements being a typical example).

- Your financial situation may have changed, affecting your ability to make loan repayments.

- Property values may have fallen.

Before you sell

Talk to your bank first. That way, you’ll be fully informed about how much of your borrowing it wants to be repaid. Bear in mind you may have to pay an early repayment charge if the bank makes you reduce your remaining loan and you have to break a fixed rate loan to do so. See also our Quick Guides:

- Early repayment charges

- Complaining about a loan decision

- Loan-to-value lending restrictions

Talk to the bank and get fully informed about how much of your borrowing it wants to be repaid before you sell.

Misunderstanding over new loan did not result in actual loss

Morgan's business needed more capital. She decided to sell her house and buy a cheaper one to reduce loan repayments and release capital for her business. She sought bank advice on what to do. It told her she might have difficulty getting a new loan after selling her house and repaying her home loan because her business was new and its income uncertain. However, the bank said it would consider accepting a new property as security for her existing loan if she settled the sale of her house and the purchase of a new one on the same day.

CASE 2Restrictions no basis for keeping entire sale proceeds

Lee owned two properties funded through separate bank loans. When he sold property A, he thought he would repay the loan on it and keep the extra money. But the bank repaid the loan in full and used the remaining sale proceeds to reduce the other loan. When queried, the bank said it had to do this because Reserve Bank restrictions required the loan-to-value ratio on the remaining property to be less than 80 per cent.

CASE 3Poor communication led to sale proceeds misunderstanding

Tama and his partner lived in Australia and owned three properties in New Zealand, two of them apartments they rented and the third a piece of bare land.

Concerns about lending decisions

We receive complaints about banks both refusing to lend and allowing customers to borrow when the customers say they could never have afforded the repayments.

Lending decisions are usually a matter of commercial judgement for banks, something beyond our powers to investigate. We can, however, investigate administrative errors in the lending application process. This includes complaints about a re…

Transferring credit card debts

Transfer processYou must apply for a credit card account at the new bank if you don't have one there already. You will be assessed against the bank’s credit criteria. Check your debt before you apply to ensure it includes purchases or payments since your last statement. Note that interest accrued during the current month may not show up.

If the bank approves your application, it will pay off your…

Early repayment charges

Customers who borrow money at a fixed interest rate for a fixed term enjoy the benefit of knowing exactly what their repayments will be over the period of the loan. They are not affected by any rise or fall in interest rates during that time. In return, banks get a pre-determined return on their money.

But if customers repay their loan early (or make a significant lump sum payment before the end …

Updated February 2022