The loss or theft of a credit or debit card can be worrying and inconvenient. But if someone also gets your PIN, you face an even greater risk of losing money. Banks typically cover any loss if you take reasonable care of your card and PIN and report any loss promptly. If you haven’t taken reasonable care, you are unlikely to recover the money. Protecting your cards and PINs is therefore vital, as is selecting a secure PIN and knowing what to do if you lose a card.

Reasonable care

You need to take reasonable care of your cards, much as you do with wallets and keys. You don’t need to know the exact location of your cards at all times, but you should know their general whereabouts, such as at home, in your bag or in your pocket. You shouldn’t leave cards unattended in a wallet or purse, or anywhere a thief could remove them without being noticed.

It is not reasonable to leave your card:

- inside a car

- in a jacket pocket when the jacket is unattended in a public place, like a café

- in a hotel when you are out (unless it is in a hotel safe).

Remember to remove your card when using it at an ATM, shop, restaurant or any other outlet after making a purchase.

Losing a card

If you can’t find your card, tell your bank as soon as possible. Banks have dedicated phone lines to report lost or stolen cards. If you are overseas, keep a note of the phone number with your travel documents.

Limiting access

You can specify the accounts that are linked to a card. The fewer a thief or scammer can access, the lower any potential loss will be. Talk to your bank about which accounts should not have card access.

Selecting PINs

Follow these tips when making up a PIN:

- Avoid obvious number combinations or sequences (for example, 1234 or 0000).

- Avoid using birthdays, anniversaries, home addresses, parts of your phone number or other numbers easily connected with you.

- Avoid sequences that also form part of your card number.

- Use a different PIN for every card.

Protecting your PIN

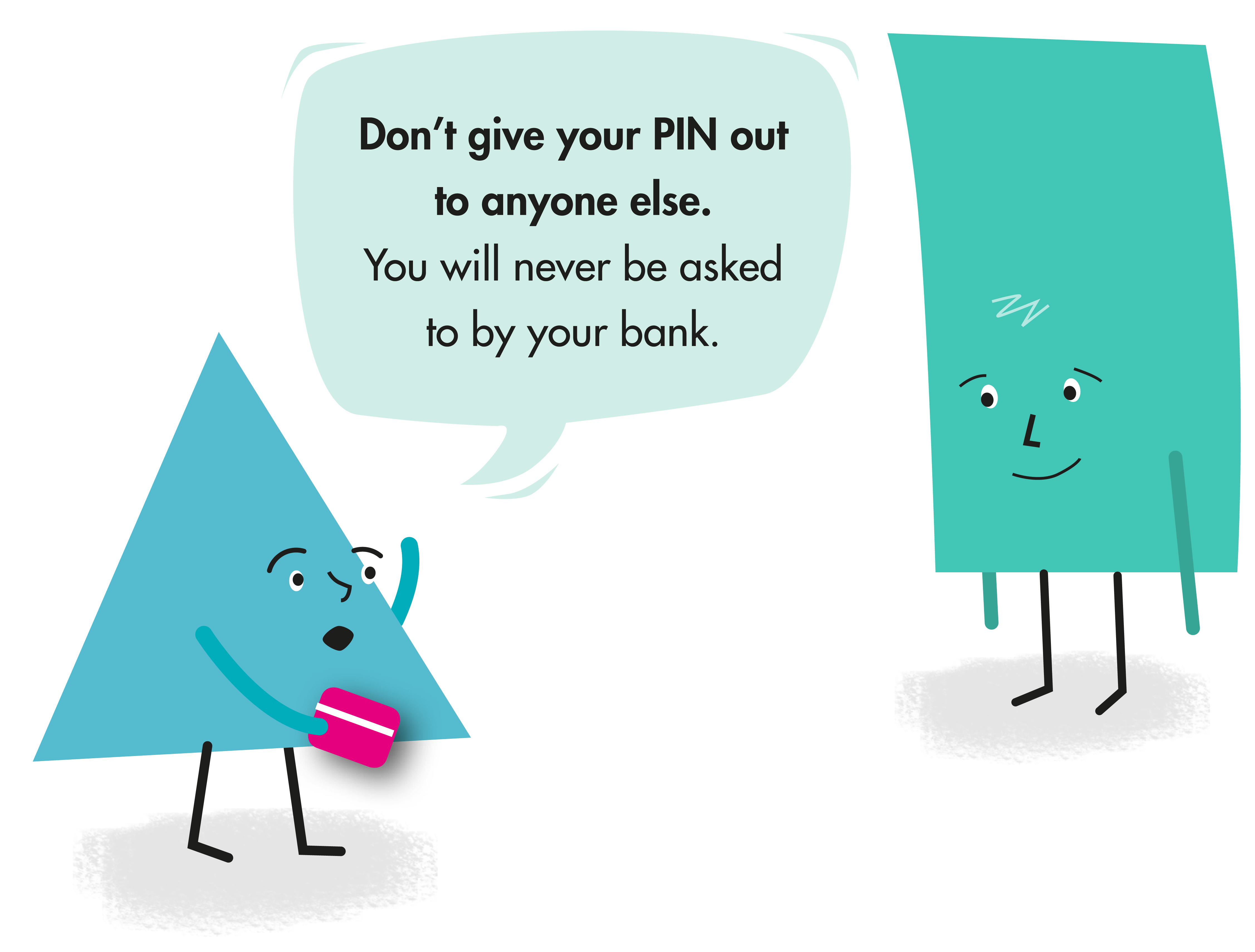

Commit it to memory and never write it down. Don’t tell anyone your PIN – and that includes family members, police or bank staff. Note that banks will never ask for your PIN. Never reply to any email asking for your PIN (or asking you to update your PIN). It’s bound to be fraudulent.

Never store your PIN (even in disguised form) on any device, including mobile phones, computers, tablets or other electronic devices. If you have done so already, delete it and get a new PIN.

You should take reasonable care when entering your PIN at an ATM or an eftpos machine in a shop so as to stop someone from seeing it. If you think someone may know your PIN, contact your bank immediately and get a new one.

The bank will typically cover your losses if you have taken reasonable care of you card and PIN and promptly reported the lost or stolen card.

Bank accepted CCTV footage as compelling evidence when we intervened

In November 2023, Lily lost her wallet, which had her credit card in it. By the time she realised later in the day that her wallet was missing, someone had already found it and used the credit card to make purchases totalling $1,500. Some purchases were made online and some at stores in a mall where she worked.

CASE 2Bank followed instructions in refixing loan for same period as interest-only payments

In August 2021, Manaia asked the bank for a two-year extension to the interest-only period on his home loan. He also asked about fixing the interest rate for a period of three to four years. The bank agreed to the extension request, but said it could not fix a rate for any longer than an interest-only period. This meant that, in his case, it could not fix a rate for more than two years. Manaia agreed to refix at a two-year interest rate and to pay interest only for the same period.

CASE 3Bank right to reject claim because PIN was easily guessable

Fern was overseas when her house was burgled in April 2022 and three of her EFTPOS cards were stolen. Fern used the same PIN for all three cards. After just two failed attempts, the offender successfully guessed the PIN and made numerous transactions using the cards totalling $32,000. When Fern discovered the transactions, she immediately called the bank.

Contactless cards

Contactless cards are a quick and easy way to make payments without the need to swipe a card or enter a PIN. Users simply hold the card close to a contactless terminal. Purchases up to $200 can be made in this way. Transactions over this amount require a PIN. Banks are automatically issuing new or replacement cards with contactless technology.

AdvantagesThey're convenient and easy to use. And the…

Travel cards

By default, money loaded on to New Zealand-issued cards is New Zealand dollars. It can then be converted to the foreign currency or currencies you need on your travels. Most cards let you have funds in several currencies at once. You can generally load money on to a travel card at a branch or online. Processing loads done via internet banking may take two or more days.

If you bought your travel c…

Chargebacks

If you make a payment with a credit or debit card through the Visa or MasterCard payment platform, you can ask your bank to charge the transaction back to the merchant’s bank, which will then debit the merchant’s account. Note: payments processed through EFTPOS cannot be charged back. You have no automatic right to demand a chargeback, but it is industry practice to charge back disputed transactio…

Updated December 2024